Defining the Future of Digital Finance: Deconstructing the New Paradigm of Capital Markets in the AI Agent Era

Author: Han Guanchao

Affiliation: Faculty of Law & Faculty of Social Sciences & School of Computing and Data Science, The University of Hong Kong

Executive Summary

The concept of migrating the bedrock of capital markets—the Initial Public Offering (IPO)—entirely onto blockchain finance has seen various ebbs and flows over the past few years. However, dismissing it as merely another overhyped technological buzzword may mean missing a profound paradigm shift. This article does not aim to provide a definitive verdict on the feasibility of "On-Chain IPOs." Instead, it seeks to step back as an objective observer and examine the fundamental shifts in the macro environment, technological realities, and commercial logic underpinning this vision today.

Figure 1: Blockchain Finance Ecosystem — A comprehensive visualization of how blockchain technology integrates with traditional financial systems, showing the interconnected network of participants, protocols, and digital assets that form the foundation of on-chain financial infrastructure.

Chapter 1: The Context of the Era—Why Now?

From an observer's perspective, the realization of any financial innovation requires the alignment of "the right time, the right place, and the right people." The transition of "On-Chain IPOs" from a distant futuristic concept to a serious topic of discussion is driven by three structural changes at the macro level.

1.1 Macro Premise I: The Rise of On-Chain Native Currencies

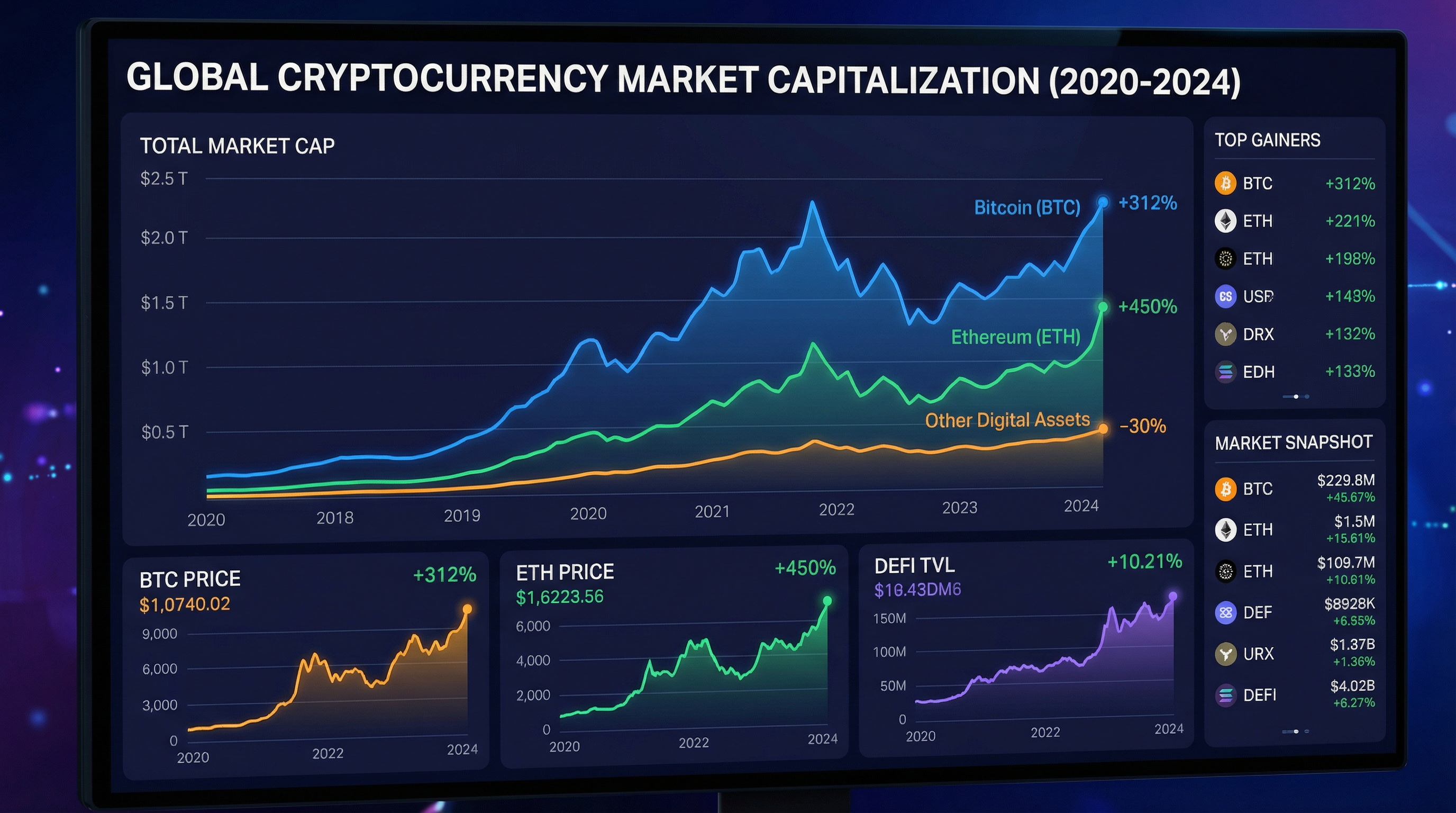

A noteworthy phenomenon is that on-chain native currencies, represented by stablecoins, have reached an economic scale that cannot be ignored. According to a report by Artemis Analytics, the annual on-chain transaction volume of stablecoins approached $9 trillion in 2025.

For comparison, Visa, the world's largest payment network, disclosed a global transaction volume of approximately $16 trillion in its FY2025 annual report. This suggests that an on-chain clearing and settlement network—operating 24/7 and independent of the traditional banking system—has reached a tipping point in capacity and market acceptance, laying the groundwork for more complex financial activities such as IPOs.

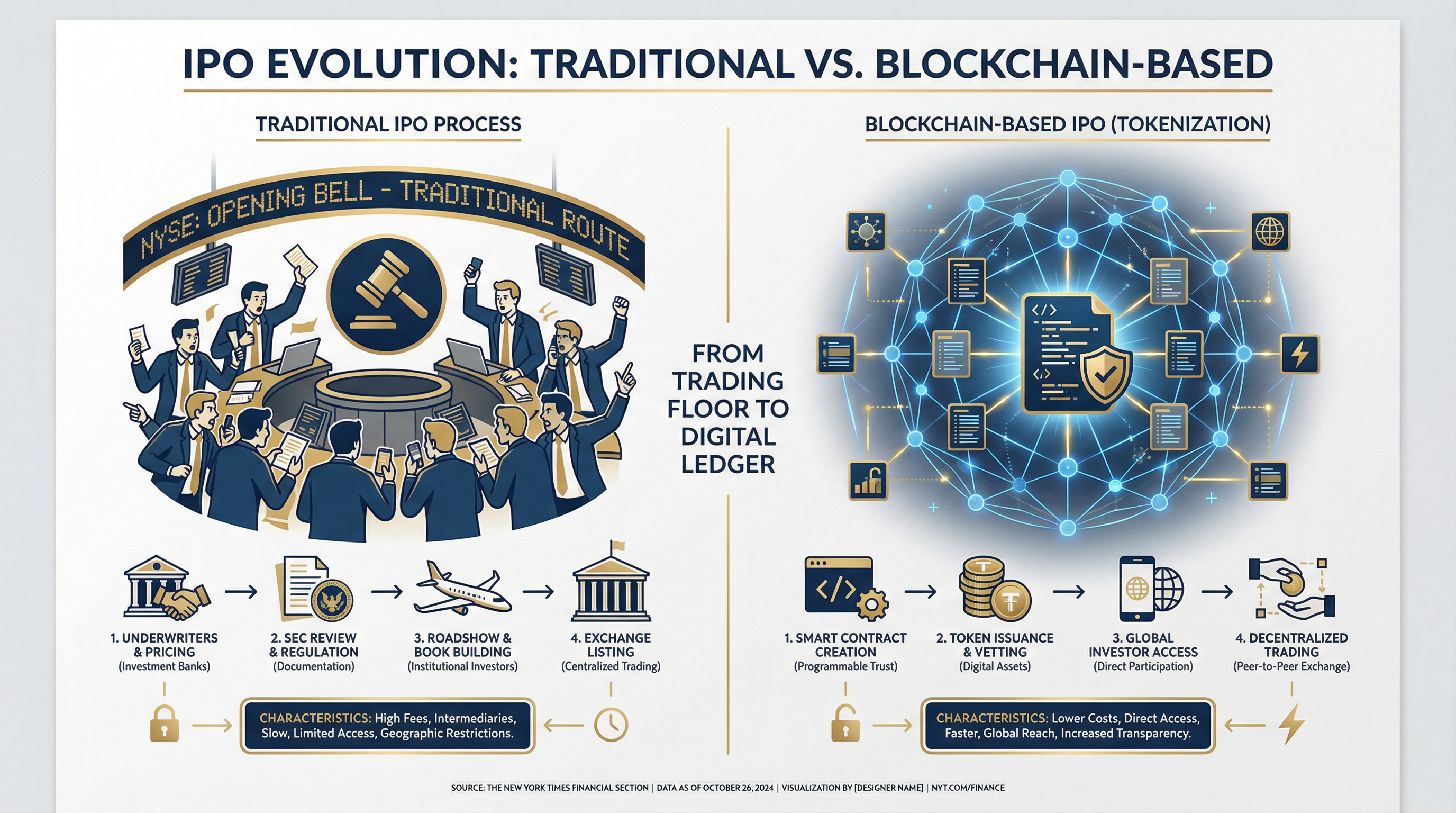

Figure 2: Traditional IPO vs. On-Chain IPO Comparison — A detailed analysis showing the fundamental differences between conventional IPO processes and blockchain-based alternatives, highlighting improvements in speed, cost, accessibility, and transparency.

1.2 Macro Premise II: Clarification of Regulatory Frameworks

Another significant change is that the regulatory stance of major global economies toward digital assets has shifted from early "blanket" crackdowns to more nuanced "classified regulation." In 2025, the United States signed the Guiding and Establishing National Innovation for U.S. Stablecoins Act (GENIUS Act) into law, formally bringing USD stablecoin issuance under federal banking supervision. The European Union's Markets in Crypto-Assets Regulation (MiCA) has also come into full effect.

Figure 3: Hong Kong as a Global Financial Hub — A visualization of Hong Kong's strategic position in the global financial ecosystem, showing its role as a bridge between Eastern and Western markets, and its potential as a leader in digital financial innovation.

1.3 Macro Premise III: Strategic Entry of Traditional Financial Institutions

While the first two points represent changes in the external environment, the shift in attitude among traditional financial giants serves as a stronger endogenous signal. A landmark event occurred in October 2025, when NASDAQ formally submitted a filing to the U.S. Securities and Exchange Commission (SEC) to amend its rules to support the listing and trading of tokenized securities. This is no longer a "fringe experiment" by an innovation department; it is a core strategic move concerning the future of the exchange.

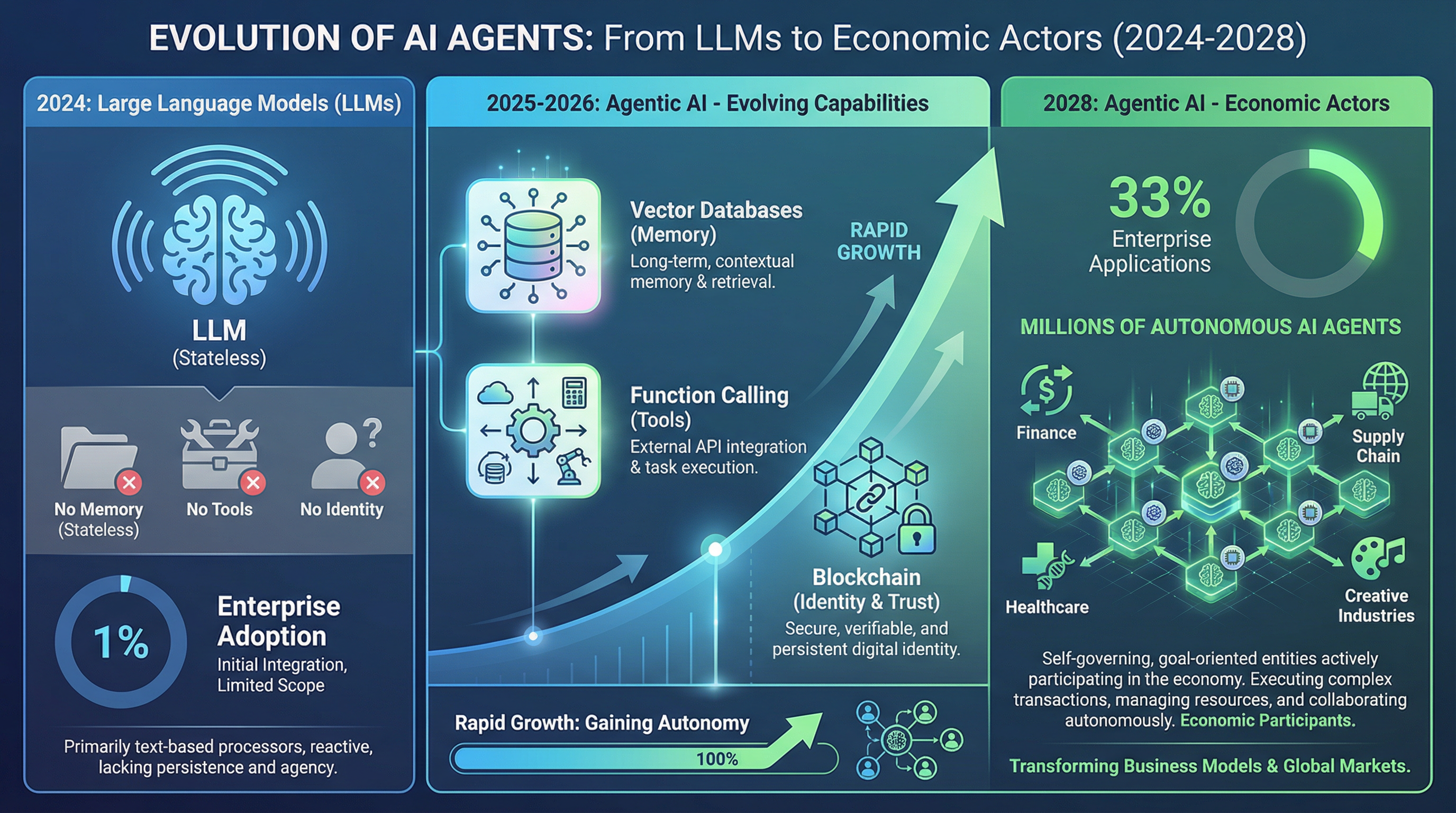

1.4 An Observation on AI Agents

However, the validity of the three macro premises above stems not from technology itself, but from a more fundamental phenomenon: the rapid influx of AI Agents into the digital economy. From an observer's perspective, this is not a niche technical trend but a profound transformation of the entire digital finance ecosystem.

Figure 4: Cryptocurrency Market Growth & AI Agent Activity — A comprehensive chart showing the exponential growth of cryptocurrency markets, stablecoin adoption, and the increasing role of AI Agents in driving transaction volumes and market efficiency.

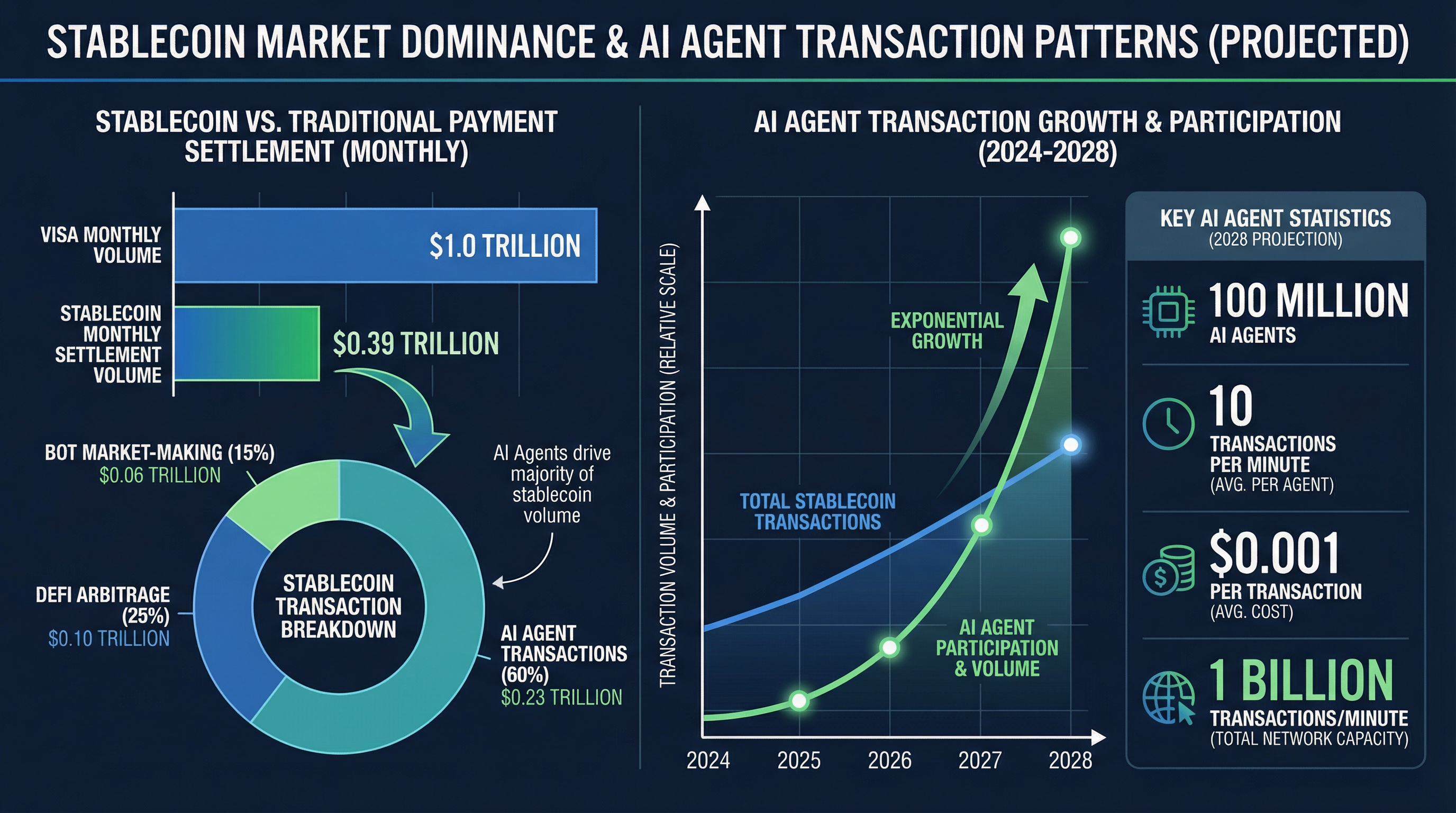

According to Coinbase's latest report, monthly stablecoin settlement volume has reached $0.39 trillion, rivaling the scale of traditional payment networks. A significant portion of these transactions originates from automated trading by AI Agents, arbitrage between DeFi protocols, and automated market-making by bots. Meanwhile, Postman statistics show that global API calls are growing by over 30% annually, and the Robotic Process Automation (RPA) market is expected to reach $25 billion in 2025. More critically, Gartner predicts that by 2028, 33% of core enterprise applications will involve Agentic AI—a 30-fold increase in just four years from less than 1% in 2024.

This implies that hundreds of millions of autonomous AI Agents are set to become the primary actors in the digital economy. Their trading strategies differ from humans—every single transaction might be minuscule. Suppose 100 million AI Agents run simultaneously, each generating ten $0.001 payments per minute; that would result in 1 billion transactions and $1 million in flow every minute. The traditional financial system cannot sustain such high-frequency, micro-scale activity. This is why Web3 infrastructure is not an option, but a necessity.

Figure 5: AI Agent Evolution and Web3 Infrastructure — Demonstrates how AI Agents are evolving from Large Language Models (LLMs) in 2024 to Agentic AI with capabilities in 2025-2026, and finally to autonomous economic actors by 2028. This evolution makes Web3 infrastructure not optional but essential.

Chapter 2: Deconstructing Technical Feasibility—Ideals, Realities, and Trade-offs

Migrating a financial activity as complex as an IPO entirely to the blockchain requires a robust, compliant, and future-proof technical architecture. From an observer's perspective, we should not merely marvel at idealistic labels like "decentralization" or "immutability," but rather examine the various trade-offs and compromises necessitated by real-world implementation. This chapter will first deconstruct the core components of this architecture through a table, followed by an in-depth analysis of the technical and governance challenges inevitable in the real world.

2.1 Core Technical Architecture: The Four Pillars

A fully functional on-chain IPO platform can be understood as four interdependent layers. The table below outlines these "Four Technical Pillars," their core functions, and their interrelationships:

| Technical Pillar | Core Function | Role in IPO |

|---|---|---|

| 1. Blockchain Layer | Distributed Ledger & Consensus | Provides the "Single Source of Truth" for ownership and transactions. |

| 2. Smart Contract Layer | Programmable Business Logic (e.g., ERC-3643) | Automates issuance, dividend distribution, and compliance |

| 3. Stablecoin Settlement Layer | Value Exchange Medium | Enables instant, atomic settlement of assets against currency. |

| 4. Oracle Interface | Off-Chain Data Bridge | Connects on-chain assets with real-world data (e.g., stock prices, KYC status). |

Four Technical Pillars

Click on each pillar to explore the technical architecture

Blockchain Layer

Distributed Ledger & Consensus

Smart Contract Layer

Programmable Business Logic

Stablecoin Settlement

Value Exchange Medium

Oracle Interface

Off-Chain Data Bridge

Data Flow Architecture

Issuance

Company submits IPO application via smart contracts

Settlement

Stablecoin settlement layer processes transactions

Verification

Oracle interfaces verify KYC/AML and market data

Recording

Blockchain layer records all transactions immutably

Figure 5: Smart Contract Security Architecture — An in-depth visualization of the multiple layers of security mechanisms protecting smart contracts, including code audits, formal verification, multi-signature wallets, and emergency governance protocols.

2.2 A Critical Examination of the Four Pillars

A mature observer must recognize that while each pillar brings disruptive advantages, they also carry profound internal contradictions and limitations.

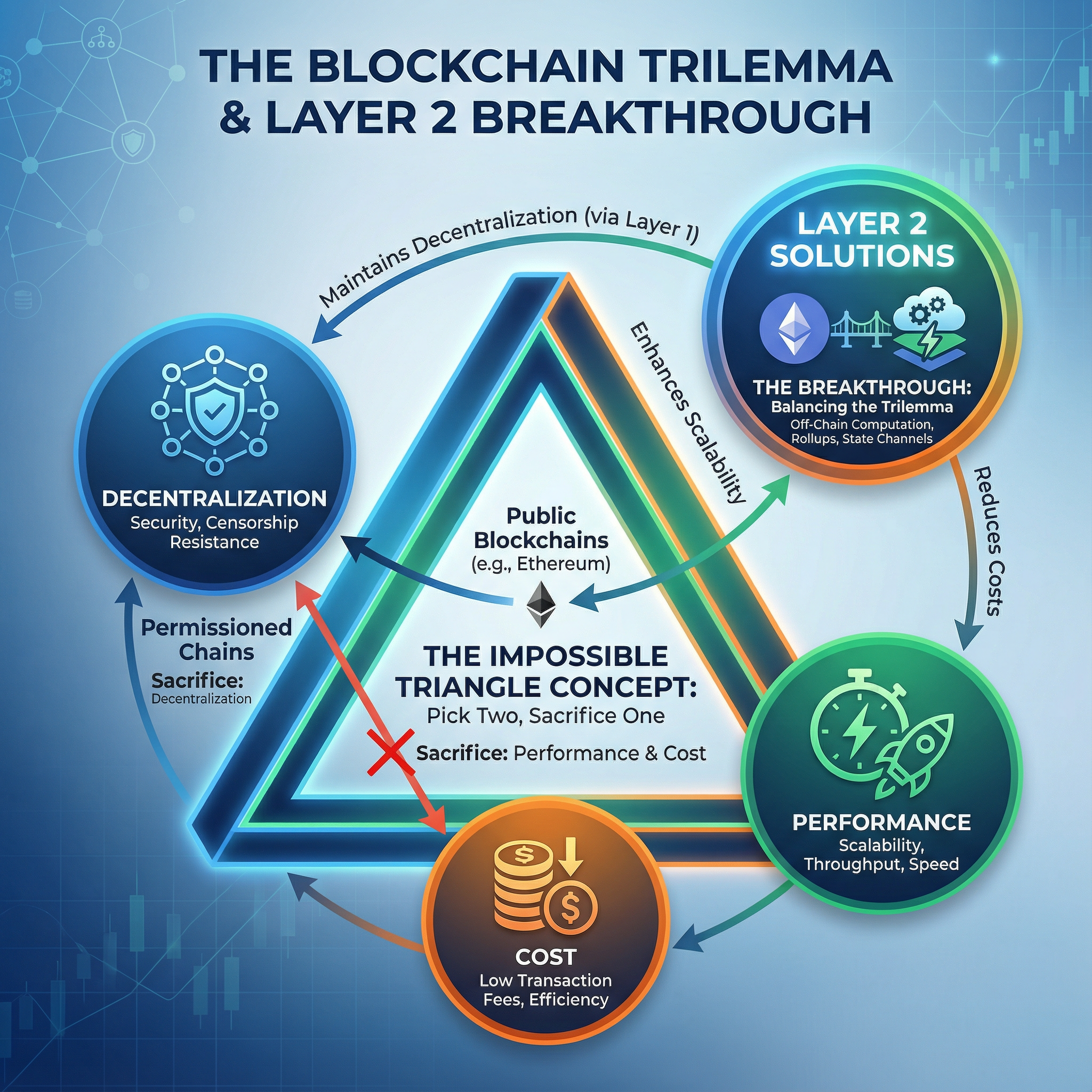

Figure 6: Blockchain Trilemma and Layer 2 Breakthrough — Visualizes the impossible trinity of blockchain systems—decentralization, performance, and cost—and how Layer 2 solutions attempt to break through this constraint.

This is the foundation of trust. However, the "Impossible Trinity"—the inability to simultaneously achieve perfect decentralization, extreme performance, and ultra-low cost—is vividly apparent here. Public chains (like Ethereum) offer the highest transparency and censorship resistance, but transaction fees can skyrocket during congestion. Consortium chains offer better performance, but their "permissioned" nature fundamentally weakens the value proposition of decentralization. Thus, any choice is a trade-off; no perfect base layer exists.

This is the core of business logic automation. However, as Mr. Li Guoliang pointed out in his lectures, a blind faith in "Code is Law" is dangerous. Once deployed, smart contracts are rigid and unquestionable. Yet, the real financial world is full of exceptions and human errors. An unfixable bug could lead to catastrophic, irreversible losses.

Therefore, a mature on-chain IPO system must abandon the fundamentalist obsession with "immutability" and introduce upgradeable contract frameworks and emergency governance mechanisms. But this raises a new question: who controls these "backdoors"? This increases rather than decreases governance complexity.

This is the "blood" that ensures smooth value flow. However, reliance on USD stablecoins effectively places the lifeblood of on-chain finance in the hands of U.S. regulators and a few issuers. The U.S. GENIUS Act, by mandating that stablecoin reserves be tied to U.S. Treasuries, has cleverly turned stablecoins into a new tool for reinforcing dollar hegemony. This over-reliance on a single sovereign currency poses severe geopolitical risks.

This is the "nervous system" connecting the on-chain world with reality. Yet, oracles are a frequently overlooked point of centralization. No matter how decentralized a blockchain system is, if it relies on a single centralized API for its data, the system's credibility is only as good as that interface.

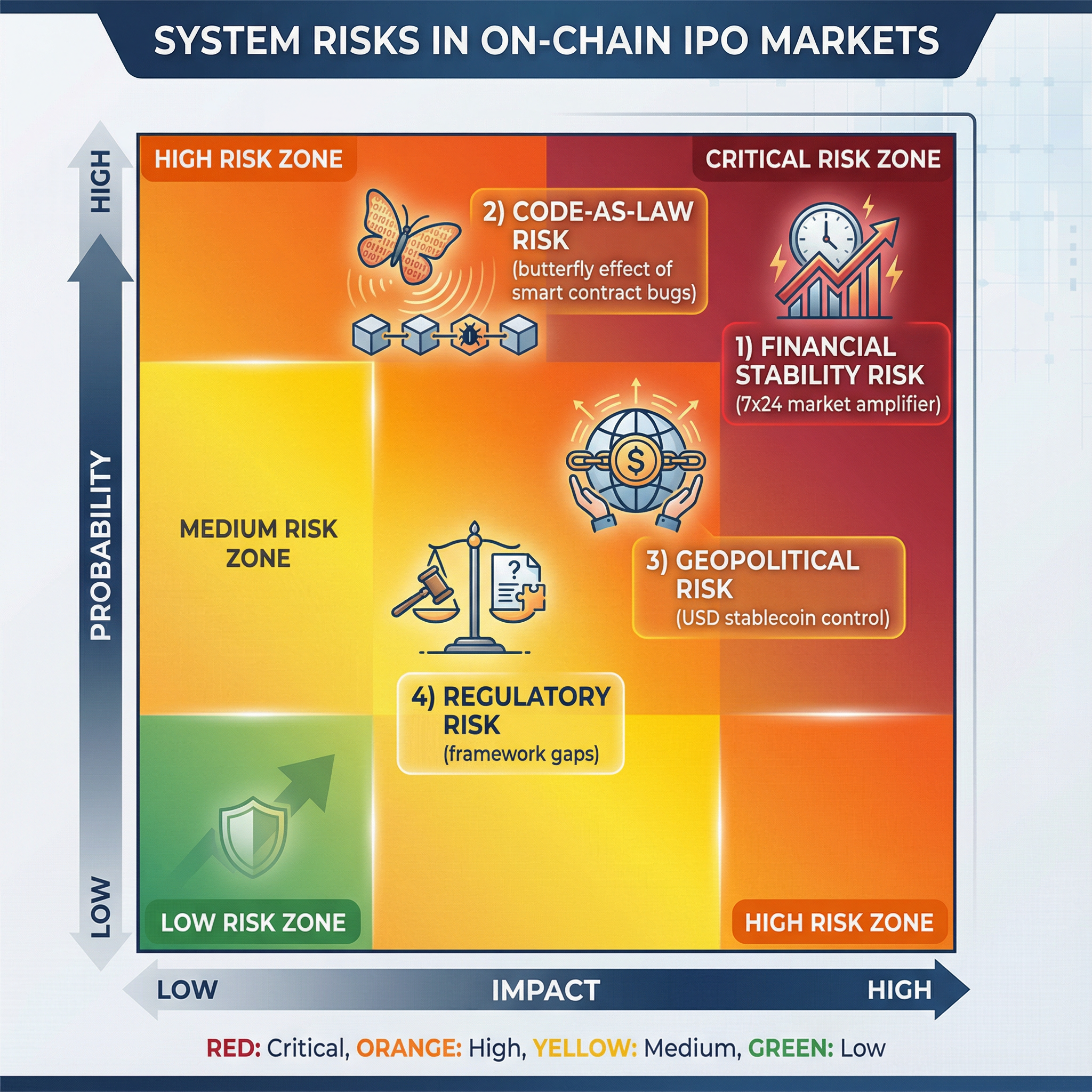

Figure 8: Systemic Risk Matrix in On-Chain IPO Markets — Risk matrix showing four major systemic risks: financial stability risk (7x24 market amplifier), code-as-law risk (butterfly effect), geopolitical risk (USD stablecoin control), and regulatory risk.

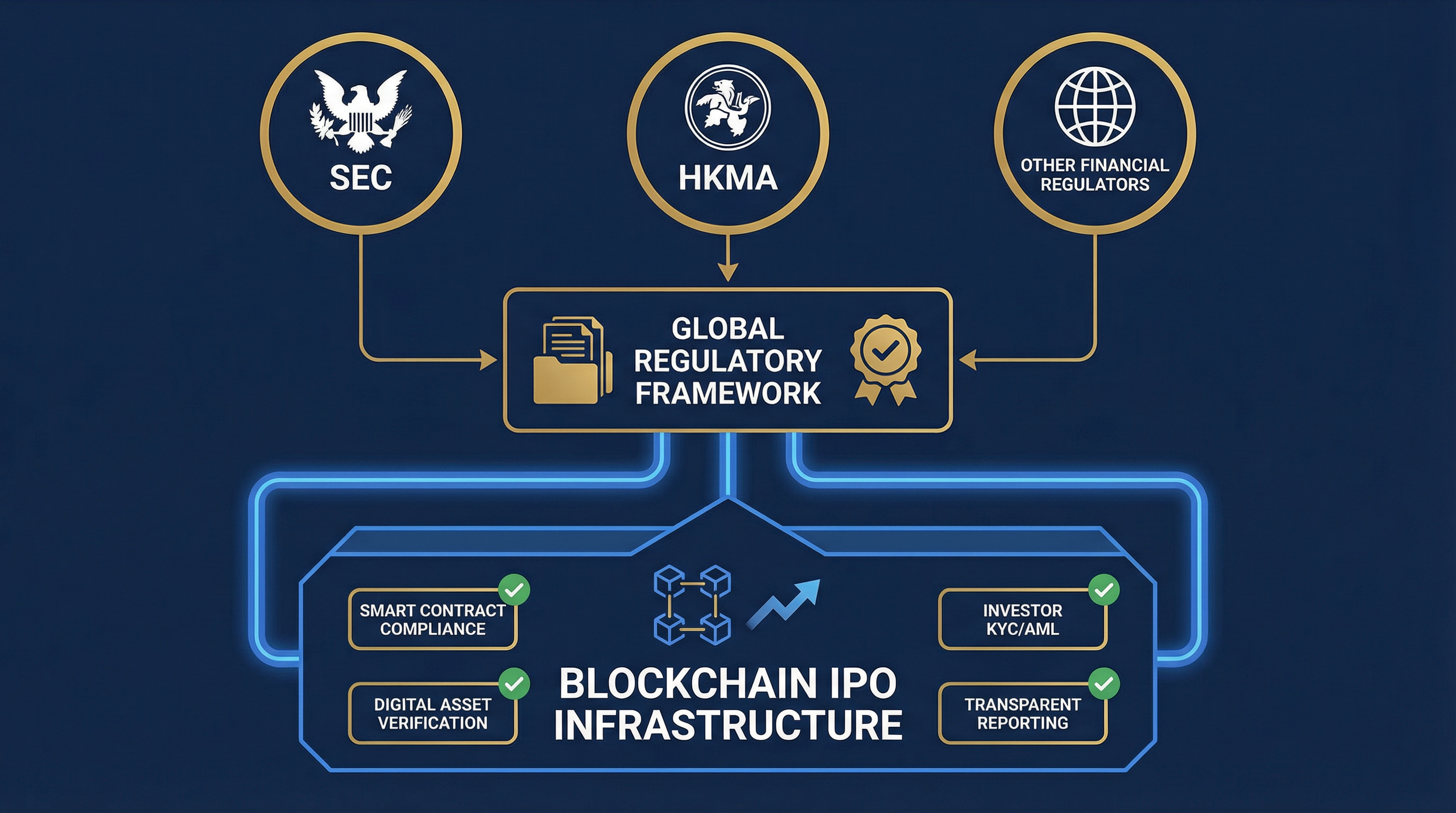

Figure 9: Global Regulatory Framework for Blockchain IPOs — A comprehensive diagram showing how major financial regulators (SEC, HKMA, FCA, etc.) are developing frameworks to govern blockchain-based securities offerings, including compliance requirements, investor protection measures, and market surveillance mechanisms.

2.3 The Evolution of AI Agents and Web3 Infrastructure

The necessity of the aforementioned technical architecture stems not only from the complexity of the IPO process itself but also from a more fundamental phenomenon: the evolution of AI Agents. This is the key to understanding "why now."

Traditional Large Language Models (LLMs) suffer from three fatal limitations. First is statelessness—each conversation starts from scratch, unable to remember user identity and historical interactions. Second is lack of tools—they can only generate text, unable to execute code or call external APIs. Third is lack of identity—they cannot represent any legal entity for signing or asset management.

However, the Agentic AI of 2026 is breaking these barriers. Through vector databases, they achieve private memory; through Function Calling and MCP, they gain tool-calling capabilities; through blockchain, they obtain verifiable on-chain identity. This means AI Agents are evolving from "conversational tools" into "economic actors."

Figure 7: Stablecoin Market Dominance and AI Agent Trading Patterns — Shows how stablecoin monthly settlement volume approaches Visa levels, and how AI Agents drive 60% of on-chain transactions, with exponential growth from 2024 to 2028.

This transformation brings a profound consequence: traditional internet and financial infrastructure were not designed for this shift. When AI Agents need to manage assets, sign contracts, and execute payments on behalf of enterprises or individuals, three fatal problems emerge:

Identity Fraud Risk: Traditional HTTP protocols have no mechanism to verify whether a request originates from a human or AI, from Company A or Company B's AI. This leaves enormous gaps for corporate espionage and impersonation.

Behavior Untraceability: In traditional systems, AI actions lack permanent, publicly verifiable audit trails. Blockchain's immutability provides AI with permanent, publicly verifiable logs of every action.

Transaction Volume Insufficiency: The scale is staggering. Assume 100 million AI Agents running simultaneously, each generating 10 transactions per minute at $0.001 each. That's 1 billion transactions per minute and $1 million flowing every 60 seconds. Traditional finance cannot handle this volume. This is precisely why Web3 infrastructure is not optional but an inevitable choice.

In essence, moving IPOs on-chain is fundamentally about enabling AI Agents to play legitimate, trustworthy, and auditable roles in capital markets. This is not a technology choice but an inevitable result of economic evolution.

Figure 7: AI-Driven Modern Trading Floor — A real-world financial trading environment showcasing how AI Agents play a critical role in modern financial markets through automated trading and real-time data analysis to drive market efficiency.

Figure 8: Multi-Screen Trading Monitoring System — Demonstrates the multi-screen monitoring systems of modern trading floors, tracking market data and trading flows in real-time, representing how traditional financial infrastructure adapts to digital transformation.

Chapter 3: Market Feasibility and Business Models

3.1 Market Demand Analysis

Market Size & Growth Trends

Real-time visualization of on-chain financial ecosystem growth

Stablecoin Trading Volume

Trillion USD

+328.6% YoY

On-Chain Asset Value

Trillion USD

+212.5% YoY

DeFi Total Value Locked

Billion USD

+1788.9% YoY

5-Year Growth Trajectory

- Stablecoin Volume

- On-Chain Assets

- DeFi TVL

Stablecoin Adoption

From $500B to $9T in 5 years

Fastest growing segment in on-chain finance

Asset Tokenization

From $200B to $2.5T in 5 years

Real-world assets moving on-chain

DeFi Ecosystem

From $100B to $850B in 5 years

Decentralized finance reaching scale

The demand for on-chain IPOs is not hypothetical. Several market signals suggest genuine demand:

- Retail Investor Accessibility: Traditional IPO allocations are heavily skewed toward institutional investors. On-chain IPOs could democratize access, allowing global retail participation in fractional shares.

- Speed and Cost Reduction: Traditional IPO processes take 6-12 months and cost $5-10 million. On-chain alternatives could reduce this to weeks and millions in savings.

- 24/7 Global Trading: Unlike traditional stock exchanges with fixed trading hours, on-chain securities can trade continuously, appealing to global investors across time zones.

3.2 Business Model Comparison: Traditional IPO vs. On-Chain IPO

Figure 9: Modern Trading Floor with Digital Transformation — A visualization of how traditional trading floors are evolving with blockchain integration, showing the convergence of legacy financial systems with decentralized finance infrastructure.

| Dimension | Traditional IPO | On-Chain IPO |

|---|---|---|

| Issuance Timeline | 6-12 months | 2-4 weeks |

| Underwriting Fees | 3-7% of capital raised | 0.5-2% |

| Geographic Reach | Primarily domestic | Global |

| Investor Base | Institutional + accredited retail | Democratized global retail |

| Settlement Time | T+2 (2 days) | Instant (atomic) |

| Regulatory Complexity | High (jurisdiction-specific) | Evolving (multi-jurisdictional) |

| Liquidity Post-IPO | Exchange-dependent | Continuous 24/7 |

| Compliance Overhead | Manual, paper-heavy | Automated via smart contracts |

3.3 Business Model Evolution: "Ecosystem as a Service" (EaaS)

Unlike traditional exchanges that rely solely on transaction fees, on-chain IPO platforms will evolve toward an "Ecosystem as a Service" (EaaS) model. The platform not only provides issuance services but seamlessly integrates issued assets into the broader DeFi ecosystem, creating multiple revenue streams.

Figure 10: Global Blockchain Adoption Map — World map visualization showing the geographic distribution of blockchain adoption, cryptocurrency trading volumes, and regulatory frameworks of major financial centers, highlighting Hong Kong's strategic position.

Key Revenue Streams for On-Chain IPO Platforms:

- Issuance Fees - Charged to companies launching on-chain IPOs (typically 0.5-2% of capital raised)

- Listing Fees - Annual or recurring fees for maintaining listings on the platform

- Liquidity Provision Incentives - Revenue from facilitating DeFi integrations and liquidity pools

- Data and Analytics - Premium access to market data, investor analytics, and trading insights

- Compliance and Custody Services - Fees for regulatory compliance, asset custody, and insurance

- Cross-Chain Bridge Services - Revenue from enabling multi-chain asset trading and settlement

This EaaS model represents a fundamental shift from the traditional exchange model. Rather than viewing the IPO as a discrete event, the platform becomes an ongoing ecosystem orchestrator, capturing value at multiple touchpoints throughout the asset lifecycle.

Chapter 4: Global Practice and Hong Kong's Strategic Opportunity

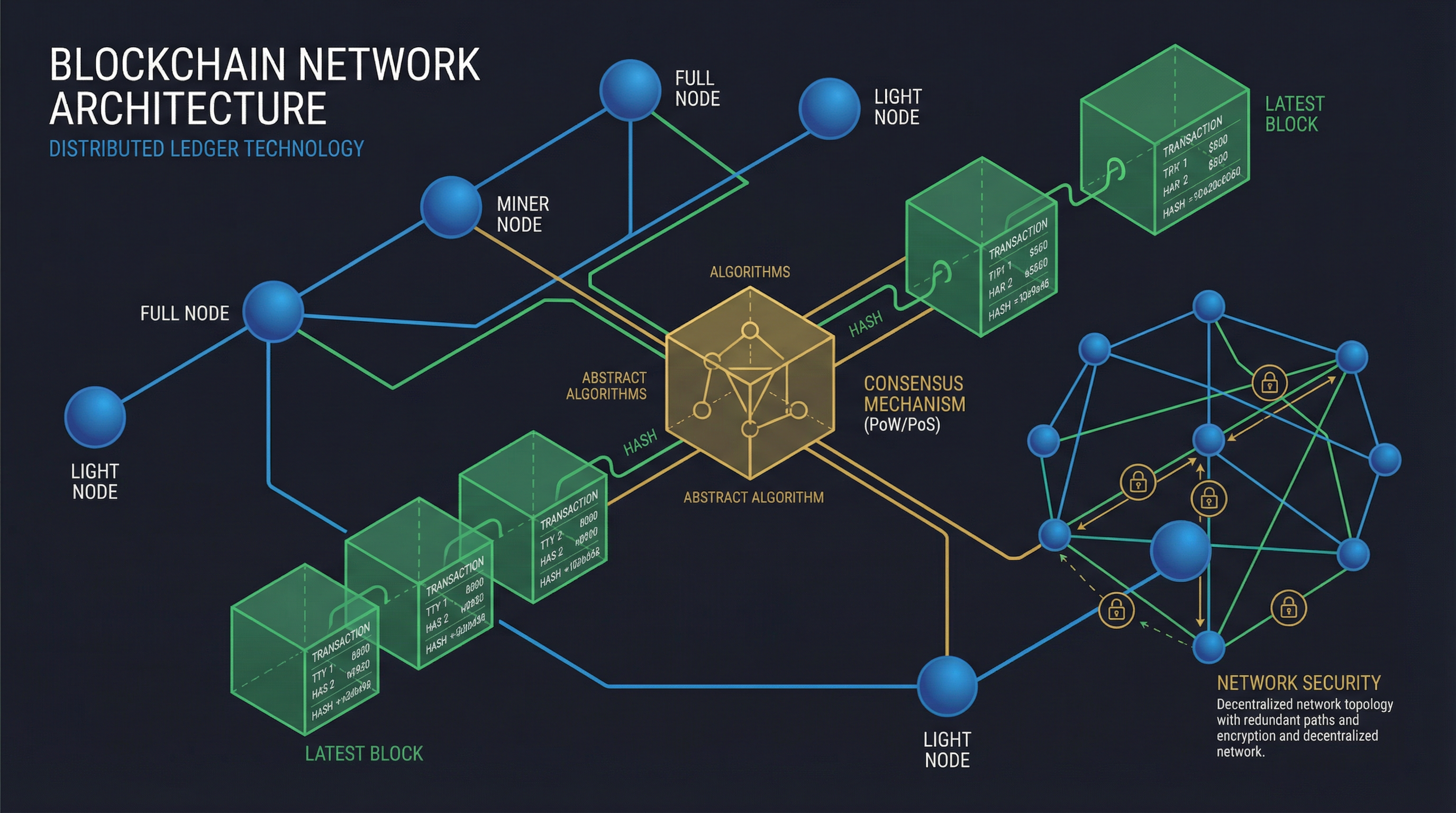

Figure 10: Blockchain Network Architecture & Security — A technical diagram illustrating the layered architecture of blockchain systems, including consensus mechanisms, cryptographic security, and distributed node networks that ensure transaction integrity and system resilience.

4.1 Regulatory Sandboxes and Pilot Programs Worldwide

Several jurisdictions are actively exploring on-chain securities:

Singapore (Monetary Authority of Singapore - MAS)

- Launched Project Ubin to explore DLT for cross-border payments and settlement.

- Approved tokenized bond issuance by financial institutions.

Switzerland (FINMA)

- Established a "Blockchain Sandbox" allowing regulated entities to experiment with tokenized securities.

- Zurich Stock Exchange (SIX) launched SIX Digital Exchange for tokenized assets.

European Union (ESMA)

- MiCA provides a harmonized regulatory framework for crypto-assets across all EU member states.

- Several EU member states are piloting tokenized government bonds.

United States (SEC)

- While cautious, the SEC has signaled openness to tokenized securities under existing securities laws.

- NASDAQ's filing suggests imminent regulatory clarity.

4.2 Hong Kong's Unique Positioning

Hong Kong possesses several structural advantages that position it uniquely for on-chain IPO leadership:

Figure 11: Hong Kong's Strategic Positioning in Digital Finance — Showcases Hong Kong's four unique advantages: "One Country, Two Systems" institutional advantage, international financial hub status, forward-looking regulatory philosophy, and geographic position as a bridge between East and West.

Institutional Advantages:

- Regulatory Sophistication: Hong Kong's Securities and Futures Commission (SFC) has decades of experience in securities regulation and has demonstrated pragmatism in adopting new technologies.

- Financial Hub Status: As a global financial center, Hong Kong has the infrastructure, talent, and institutional relationships to lead this transition.

- Bridge Between Markets: Hong Kong's unique position as a gateway between Mainland China and the West makes it ideal for a global digital asset hub.

Market Advantages:

- Mainland Capital: Access to Mainland Chinese capital seeking international diversification.

- Asian Investor Base: Proximity to Asia's fastest-growing economies and investor populations.

- Time Zone Advantage: Positioned between European and American markets, enabling 24/7 trading coverage.

4.3 Hong Kong's Roadmap: A Phased Approach

Hong Kong Three-Step Roadmap

Strategic pathway to becoming a global digital asset center

Build Stablecoin Ecosystem

Core Objectives

- •Establish stablecoin settlement infrastructure

- •Build stablecoin calculation layer

- •Create digital asset compliance framework

Expected Outcomes

- ✓Stablecoin trading volume reaches $500B

- ✓Hong Kong becomes regional stablecoin hub

- ✓Regulatory framework finalized

Timeline Progress

Conclusion: Embracing the Inevitable Future

Returning to the question posed at the beginning: Is moving IPOs on-chain feasible in today's macro and technical context?

From an observer's perspective, the answer is clear: it is not only feasible but likely an inevitable trend. We have seen that the conditions for migrating core capital market activities on-chain are largely in place, whether in terms of technological maturity, market demand scale, or the evolution of global regulatory frameworks.

More importantly, we must recognize that the driver of this transformation far exceeds technology itself. It is a structural reshaping of the global financial system in the digital age and a new round of geopolitical maneuvering in virtual space. For Hong Kong, this is both a challenge and an opportunity. The challenge lies in overcoming path dependency and balancing innovation with risk; the opportunity lies in Hong Kong's unique institutional advantages and geographical location, giving it the greatest potential to become a global digital asset center connecting East and West, and merging old and new finance.

We should no longer view "On-Chain IPOs" as a fringe, niche experiment. It represents a more efficient, transparent, and globalized way of capital formation. To embrace it is to embrace a more open and inclusive financial future. The road ahead is undoubtedly challenging, but as history has repeatedly proven, technology-driven paradigm shifts do not stop for anyone's will. The only choice is to be the one who shapes the future, rather than the one left behind by it.

Appendix: Glossary

References

[1] Artemis Analytics. (2026, January). 2025 Global Stablecoin Flow Report. [Link TBD]

[2] Visa Inc. (2026, January). Visa Inc. Reports Fiscal Full-Year 2025 Financial Results. [Official Press Release Link TBD]

[3] U.S. Congress. (2025, July 18). H.R.1122 - Guiding and Establishing National Innovation for U.S. Stablecoins Act. Congress.gov. https://www.congress.gov/bill/119th-congress/house-bill/1122

[4] Securities and Futures Commission (SFC), Hong Kong. (2023, November). Circular on Intermediaries Engaging in Tokenised Securities-related Activities. https://apps.sfc.hk/edistributionWeb/gateway/EN/circular/doc?refNo=23EC69

[5] NASDAQ. (2025, October). Notice of Filing of a Proposed Rule Change to List and Trade Tokenized Equity Securities. U.S. Securities and Exchange Commission. [SEC Official Filing Link TBD]

[6] Wu, Hao. (2026, January). Stablecoin Regulation and the Future of U.S. Dollar Hegemony. Lecture delivered at Hong Kong University. [Lecture Content Citation]

Key Data Dashboard

Stablecoin Trading Volume

9Trillion USD

On-Chain Asset Value

2.5Trillion USD

DeFi Total Value Locked

850Billion USD